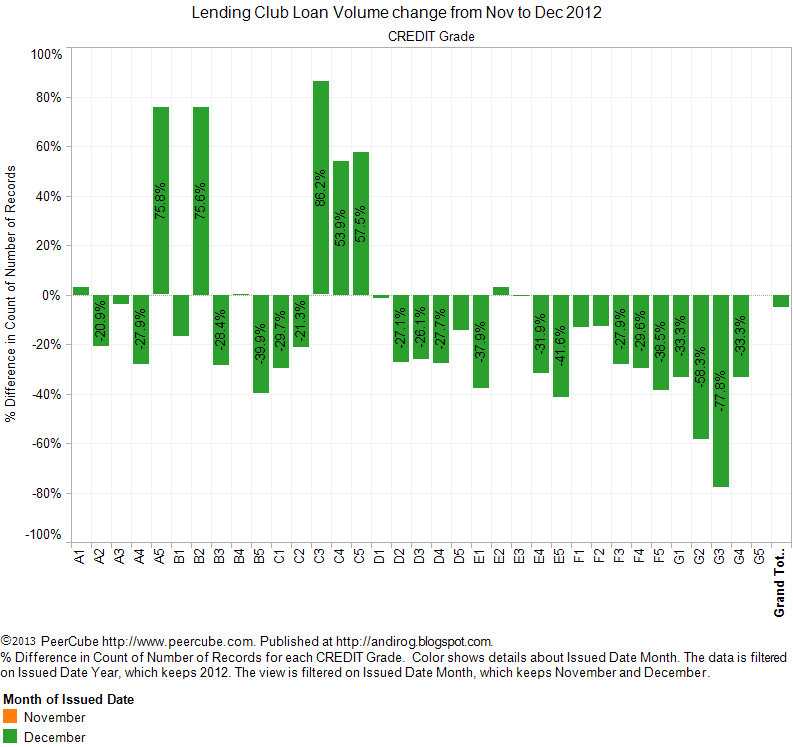

Minimum Credit Criteria

In November, Lending Club not only hide the details of underwriting process, as described in my previous post Lending Club Loans - Impact of Recent Changes, but also changed the minimum credit criteria for the borrowers. The new minimum credit criteria is much more lenient and directed at attracting lower quality borrowers.The minimum credit criteria in the latest prospectus filed in November 2012 is listed as follows:

Under the current credit policy, prospective borrower members must have among other elements:The minimum credit criteria in the previous prospectus filed in August 2012 is listed as follows:

- a minimum FICO score of 660 (as reported by a consumer reporting agency);

- a debt-to-income ratio (excluding mortgage) below 35%;

- minimum credit history of 36 months;

- 6 or less inquiries in the last 6 months; and

- at least 2 revolving trade accounts.

Under the current credit policy, prospective borrower members must have among other elements:The bold text above indicates the new condition added in the minimum credit criteria and the strikeout text above indicates the conditions removed. The new condition is nothing more than the lenient version of number of credit inquiries in the past six months.

- a minimum FICO score of 660 (as reported by a consumer reporting agency);

- a debt-to-income ratio (excluding mortgage) below 35%;

- a credit report (as reported by a consumer reporting agency)

without any current delinquencies, recent bankruptcy, tax liens or non-medical related collections opened within the last 12 months, and reflecting:- at least two accounts currently open;

for credit credits 740 and higher, no more than 8 credit inquiries on the credit report in the past six months and for credit scores below 740, no more than 3 inquiries on the credit report in the past six months;a revolving credit balance of less than $150,000;utilization of credit limit not exceeding 98%; and- a minimum credit history of 36 months.

Public Records

There was some discussion on LendAcademy forum about Increase in Applicants With Public Records. The table below shows the monthly loan volume with respect to number of public records for loans issued in 2012. In November, 127 loans were issued to borrowers who had at least one public record. The number of such loans increased to 202 in December, an increase of almost 60% over previous month.

I believe the changes in the minimum credit criteria as mentioned in November prospectus may have resulted in increase of borrowers with public records in December. No longer Lending Club excludes borrowers with current delinquencies, recent bankruptcies, tax liens, and non-medical related collections in past 12 months.

Did Lending Club modify 'proprietary' credit grade model to accommodate this change in minimum credit criteria? I was expecting the credit grade shifting to the right toward grade G for such loans. The table below shows the monthly volume and credit grade of loans issued to borrowers with more than 2 public records. There is no shift in credit grade of loans to borrowers with public records. It doesn't appear that Lending Club credit grade model accounts for the number and type of public records.

Accounts Now Delinquent

The table below shows the monthly loan volume with respect to borrowers' number of accounts currently delinquent. It is clear from the table that prior to December, Lending Club didn't issue any loans to borrowers who had delinquent accounts at the time of applying for loan. In December 2012, Lending Club issued 15 loans to borrowers who had one or two accounts delinquent at the time of loan application.

The credit grade for loans to borrowers with one account delinquent ranged from A5 to F1 while the one loan to borrower with two accounts delinquent has credit grade of F3. It is too early to determine whether Lending Club's proprietary credit grade model accounts for borrowers who have accounts delinquent currently.

Amount Delinquent

The table below shows the monthly loan volume with respect to total amount currently delinquent for borrowers. Similar to accounts now delinquent above, in December 2012, Lending Club started issuing loans to borrowers who have any amount delinquent currently. In December 2012, Lending Club issued 10 loans to borrowers who had between $25 and $65,000 amount delinquent.

Did Lending Club proprietary credit grade model account for borrowers who have any amount delinquent currently? Not a chance! Any reasonable proprietary model most likely will consider borrower with higher delinquent amount to be of higher credit risk.

See the table below that shows the credit grade of loans issued in December 2012 to borrowers who had any delinquent amount. First, there is no visible pattern between credit grade and delinquent amount. Second, which reasonable model that accounts for currently delinquent amount will assign credit grade A5 to a loan for a borrower who has $65,000 in delinquent amount versus grade F1 to a loan for a borrower who has $25 in delinquent amount? This leads me to believe that the credit grade model doesn't account for amount currently delinquent.

Key Takeaways

- Lending Club has relaxed the minimum credit criteria to attract more borrowers that most likely will result in more borrowers with higher credit risk on lending club platform.

- Lending Club proprietary credit grade model doesn't appear to account for the credit quality of the new borrowers that only became eligible since lowering of minimum credit criteria.

- Lenders may benefit by taking the 'common sense' approach to details of public record, and accounts and amount currently delinquent until sufficient historical data is captured to show the pattern and impact of such borrower attributes.

How can PeerCube help?

The loan details page on PeerCube can be of great help to lenders as it shows 71 different loan and borrower attributes including the above-mentioned attributes that may shed better light on borrower's credit quality.Below is a screen capture of PeerCube's loan detail page for a C2 credit grade loan with such attributes highlighted. Will you invest in a C2 grade loan whose borrower has one bankruptcy, two tax liens, two delinquent accountss and $5,369 amount currently delinquent?

Reviewing the loan detail page, PeerCube users can avoid loans that may be of higher risk than the assigned credit grade represents.